The New Deal-Breaker in Real Estate No One Saw Coming

Why Luxury Buyers Are Walking Away From Dream Homes in Florida, D.C., the Chesapeake Bay, and Delaware Beach Towns

The New Deal-Breaker in Real Estate Isn’t Interest Rates — It’s Insurance

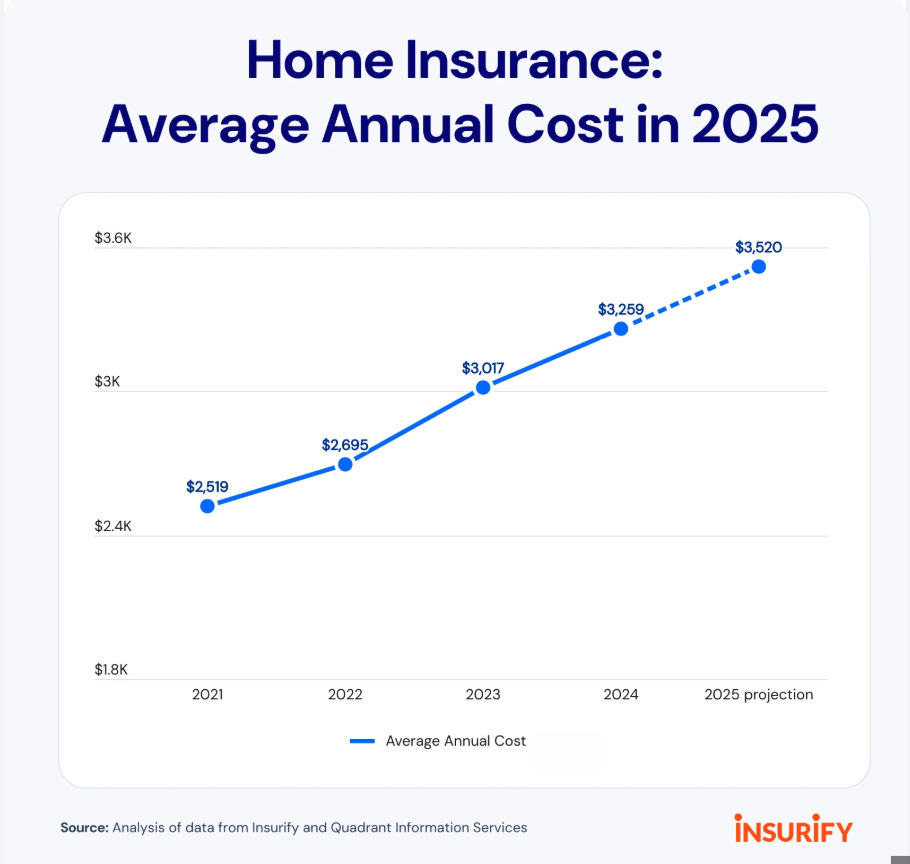

In every market cycle, there’s always a new deal-breaker. Once it was appraisals. Then it was interest rates. Now, it’s something most people never saw coming: homeowners insurance. And not the sort of incremental rate increases that quietly show up at renewal, but full-blown volatility — double-digit premium hikes year over year, shrinking coverage, and entire neighborhoods that are functionally uninsurable. Nationally, typical homeowners are now paying over 20% more in premiums than just a few years ago, with average annual costs topping $3,300 in 2024.

It’s hitting hardest in the very places people love most — Florida’s coasts, the Chesapeake Bay, Delaware’s beach towns, the riverfront pockets of greater Washington. Florida, already one of the most expensive states for home insurance in the country, now sees average premiums north of $5,800 per year, nearly double the national norm. In the Chesapeake region, a mix of low-lying land and chronic nuisance flooding has pushed more properties into higher-risk categories, forcing buyers into flood insurance they never expected to need.

Here’s what that looks like on the ground. A family in Annapolis falls in love with a classic white Colonial on the Severn — everything dialed in: dock, deep water, a kitchen made for Thanksgiving. Then the insurance quote lands: a premium in the high five figures once you factor in wind and flood, with a carrier who can walk away after a rough storm season. A cash buyer in Rehoboth offers full price for a glass-and-steel beach house, only to discover underwriting has reclassified the area under newer FEMA flood maps, driving premiums and deductibles into a range that feels less like protection and more like speculation.

In Georgetown, buyers touring townhouses near Rock Creek Park or the Potomac are hearing about water intrusion, sewer backups, and “once in a century” storms that now seem to arrive every few years. Lenders, spooked by the data, quietly tighten their own internal guidelines. In many deals, the pivotal question is no longer, “Will the house appraise?” It’s, “Can we insure it, at a number that makes sense?” Across the country, approved rate filings show homeowners’ policies rising by double digits for the second year in a row, with more than 30 states posting 10% increases or more in 2024 alone.

The reasons behind this are both obvious and opaque. Severe weather is more frequent and more expensive. Reinsurance — the insurance that insurers buy to protect themselves — has surged in cost, and those increases are passed straight through to homeowners. Carriers in high-risk states like Florida have gone insolvent or pulled back, leaving fewer players and less competition. Regulators, trying to balance consumer pain against carrier stability, are approving rate hikes at a pace that would have been unthinkable a decade ago.

For luxury buyers, the impact isn’t just financial; it’s psychological. The waterfront house on the bay, the contemporary in Miami, the gracious Victorian in a flood-prone part of Old Town — these are homes people buy as much with their hearts as with their spreadsheets. When insurance starts to look like a moving target, it introduces a layer of doubt that no staging or marketing can fully erase. Some buyers walk away, not because they can’t afford the premium, but because they don’t trust the direction of travel. Others accept the cost but quietly question the exit strategy: Will the next buyer be willing — or able — to shoulder the same burden?

“In today’s luxury market, the make-or-break moment doesn’t always happen at the negotiation table. More and more, it happens in the underwriting office.”

On our side of the table, the job description is changing in real time. Homeowners insurance used to be the last box you checked before closing. Today, it’s one of the first phone calls. Brokers are lining up boutique agencies, specialty underwriters, and flood consultants before a client ever writes an offer. We’re reading flood maps, elevation certificates, and loss histories with the same intensity we once reserved for appraisal reports. In markets along the Chesapeake Bay, where land elevation is among the lowest in the country, flood exposure and insurance requirements are now inseparable from valuation.

Sellers are being pulled into this new reality as well. A stunning waterfront property that has not been thoughtfully hardened against risk — raised systems, improved drainage, smart materials — is now competing not only on view and finishes, but on insurability. In some states, secondary homes and frequently flooded properties are seeing annual increases in flood insurance of up to 25%, a pace that can quickly outstrip rental income or second-home budgets. Savvy owners are starting to invest in resilience, not just to protect their property, but to protect their buyer pool.

There is a larger story unfolding here about climate, regulation, and capital markets, and it will take years to fully play out. But for now, at the level where clients sign contracts and wire deposits, the reality is simple: the cost and availability of homeowners insurance has become a primary driver of what sells, what sits, and what never even makes it to the closing table. Across many regions, homeowners’ insurance premiums have grown far faster than inflation and even outpaced the run-up in home prices themselves.

The modern luxury buyer is not just asking, “Is this a good house?” or “Is this a good price?” The sharper question — the one separating the impulsive purchase from the durable one — is, “Is this a good risk?” And increasingly, that answer is being written not in the listing remarks, but in the fine print of an insurance policy.